Understanding Government Budget Accounting

In the realm of public finance, government budget accounting plays a crucial role in ensuring transparency, accountability, and effective financial management. It involves the systematic recording, analysis, and reporting of all financial transactions related to government revenues and expenditures.

Government budget accounting serves as a tool for policymakers to allocate resources efficiently, monitor fiscal performance, and make informed decisions about public spending. By maintaining accurate records of income and expenses, governments can track their financial health and ensure that funds are used in accordance with established policies and priorities.

One key aspect of government budget accounting is the distinction between various types of budgets, such as operating budgets, capital budgets, and cash budgets. Operating budgets deal with day-to-day expenses like salaries and utilities, while capital budgets focus on long-term investments in infrastructure and assets. Cash budgets, on the other hand, track the flow of cash in and out of government coffers.

Another important concept in government budget accounting is the principle of accrual accounting, which requires transactions to be recorded when they occur rather than when cash actually changes hands. This method provides a more accurate picture of a government’s financial position by matching revenues with expenses in the same accounting period.

Transparency is a key principle in government budget accounting. Citizens have the right to know how their tax money is being spent, and accurate financial reporting helps build trust between governments and their constituents. By adhering to international standards of accounting practices, governments can enhance credibility and demonstrate their commitment to fiscal responsibility.

In conclusion, government budget accounting is a vital component of public financial management that ensures accountability, transparency, and effective resource allocation. By maintaining accurate records, following sound accounting principles, and promoting transparency in reporting practices, governments can uphold good governance standards and foster trust among citizens.

Understanding Government Budget Accounting: Key Questions and Answers

- What type of accounting is used by government?

- What are the three types of budgets in accounting?

- What is the government financial budget?

- What is a budget in government accounting?

- How to account for a budget?

- What is budget in accounting?

What type of accounting is used by government?

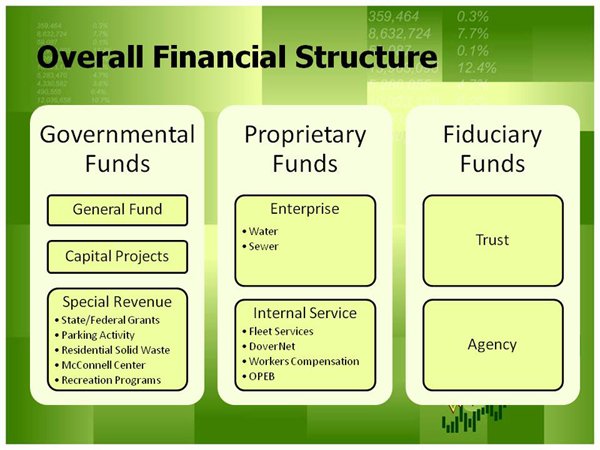

In government budget accounting, the type of accounting commonly used is known as fund accounting. Fund accounting is a specialised form of accounting that is tailored to the unique financial structure and reporting requirements of governmental entities. Unlike traditional corporate accounting, which focuses on profit and loss, fund accounting segregates financial resources into different funds or accounts based on their intended purpose or restrictions. This approach enables governments to track and report on the use of public funds with clarity and transparency, ensuring that each fund is managed in accordance with specific regulations and guidelines.

What are the three types of budgets in accounting?

In the realm of government budget accounting, there are three main types of budgets that play a pivotal role in financial planning and management. The first type is the operating budget, which focuses on day-to-day expenses such as salaries, utilities, and supplies. The second type is the capital budget, which deals with long-term investments in infrastructure and assets to support economic growth and development. Lastly, the cash budget tracks the flow of cash in and out of government coffers, ensuring that there is enough liquidity to meet financial obligations. Understanding these three types of budgets is essential for governments to effectively allocate resources, monitor fiscal performance, and make informed decisions about public spending.

What is the government financial budget?

The government financial budget refers to a comprehensive plan that outlines the expected revenues and expenditures of a government over a specific period, typically a fiscal year. It serves as a financial roadmap that guides policymakers in allocating resources, setting priorities, and managing public finances effectively. The government financial budget details how tax revenues, grants, borrowing, and other sources of income will be utilised to fund various programmes, services, and projects. By providing a clear overview of planned spending and revenue projections, the government financial budget enables transparency, accountability, and informed decision-making in the realm of public finance.

What is a budget in government accounting?

In the realm of government accounting, a budget serves as a comprehensive financial plan that outlines the expected revenues and expenditures of a government entity over a specific period, typically a fiscal year. It is a crucial tool that guides decision-making processes, resource allocation, and financial management within the public sector. Government budgets detail how public funds will be raised through taxes, grants, and other sources, as well as how these funds will be spent on various programs, services, and infrastructure projects to meet the needs of citizens. By setting clear budgetary goals and priorities, governments can ensure fiscal discipline, accountability, and transparency in their financial operations.

How to account for a budget?

When it comes to accounting for a budget in the context of government finance, several key steps need to be followed. Firstly, it is essential to establish clear budgetary guidelines and frameworks that outline revenue sources, expenditure categories, and financial goals. This initial planning phase sets the foundation for effective budget accounting. Once the budget is approved, meticulous record-keeping of all financial transactions is crucial. This includes accurately documenting revenues received and expenditures made in accordance with the allocated budget amounts. Regular monitoring and reporting on budget performance are also vital to ensure that financial resources are being managed efficiently and in line with established objectives. By adhering to these practices and maintaining transparency throughout the process, governments can effectively account for their budgets and promote responsible fiscal management.

What is budget in accounting?

In the context of accounting, a budget refers to a detailed financial plan that outlines expected revenues and expenses over a specific period. It serves as a strategic tool for organisations, including governments, to set financial goals, allocate resources efficiently, and monitor performance against predetermined targets. Budgets in accounting help in forecasting future financial outcomes, controlling costs, and making informed decisions about resource allocation. By comparing actual financial results with the budgeted figures, organisations can assess their financial health and make adjustments as needed to achieve their financial objectives.